Figma's S-1: A PLG Powerhouse

Yesterday, Figma filed its beautifully designed S-1.

It reveals a product-led growth (PLG) business with a remarkable trajectory. Figma’s collaborative design tool platform disrupted the design market long-dominated by Adobe.

Here’s how the two companies stack up on key metrics for their most recent fiscal year:

| Metric (2024) | Figma | Adobe |

|---|---|---|

| Revenue (YoY Growth) | $749M (48%) | $21.5B (11%) |

| Gross Margin | 88.3% | 89.0% |

| Non-GAAP Op Margin | 17.0% | 44.5% |

| Sales Efficiency | 1.00 | 0.39 |

| Adjusted FCF Margin1 | 24.2% | 36.6% |

| Net Dollar Retention | 132% | NA |

| Customers > $100k ARR | 963 | NA |

Figma is about 3% the size of Adobe but growing 4x faster. The gross margins are identical. Figma’s 132% Net Dollar Retention is top decile.

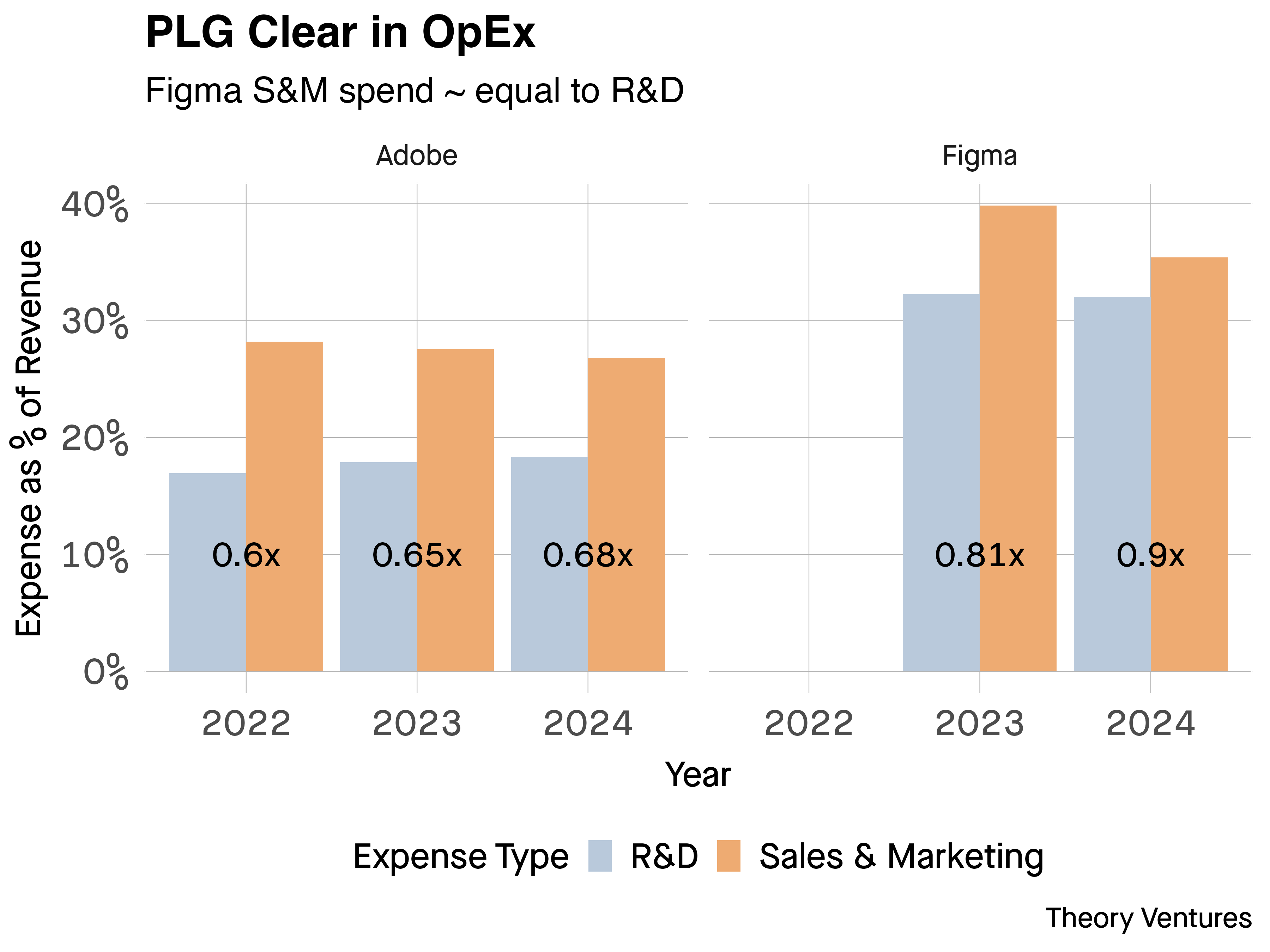

The data also shows Figma’s Research & Development spend nearly equals Sales & Marketing spend.

This is the PLG model at its best. Figma’s product is its primary marketing engine. Its collaborative nature fosters viral, bottoms-up adoption, leading to a best-in-class sales efficiency of 1.0. For every dollar spent on sales & marketing in 2023, Figma generated a dollar of new gross profit in 2024. Adobe’s blended bottoms-up & sales-led model yields a more typical 0.39.

The S-1 also highlights risks. The most significant is competition from AI products. While Figma is investing heavily in AI, the technology lowers the barrier for new entrants. Figma’s defense is its expanding platform—with products like FigJam, Dev Mode, & now Slides, Sites, & Make.

These new product categories have driven many PLG AI software companies to tens & hundreds of millions in ARR in record time.

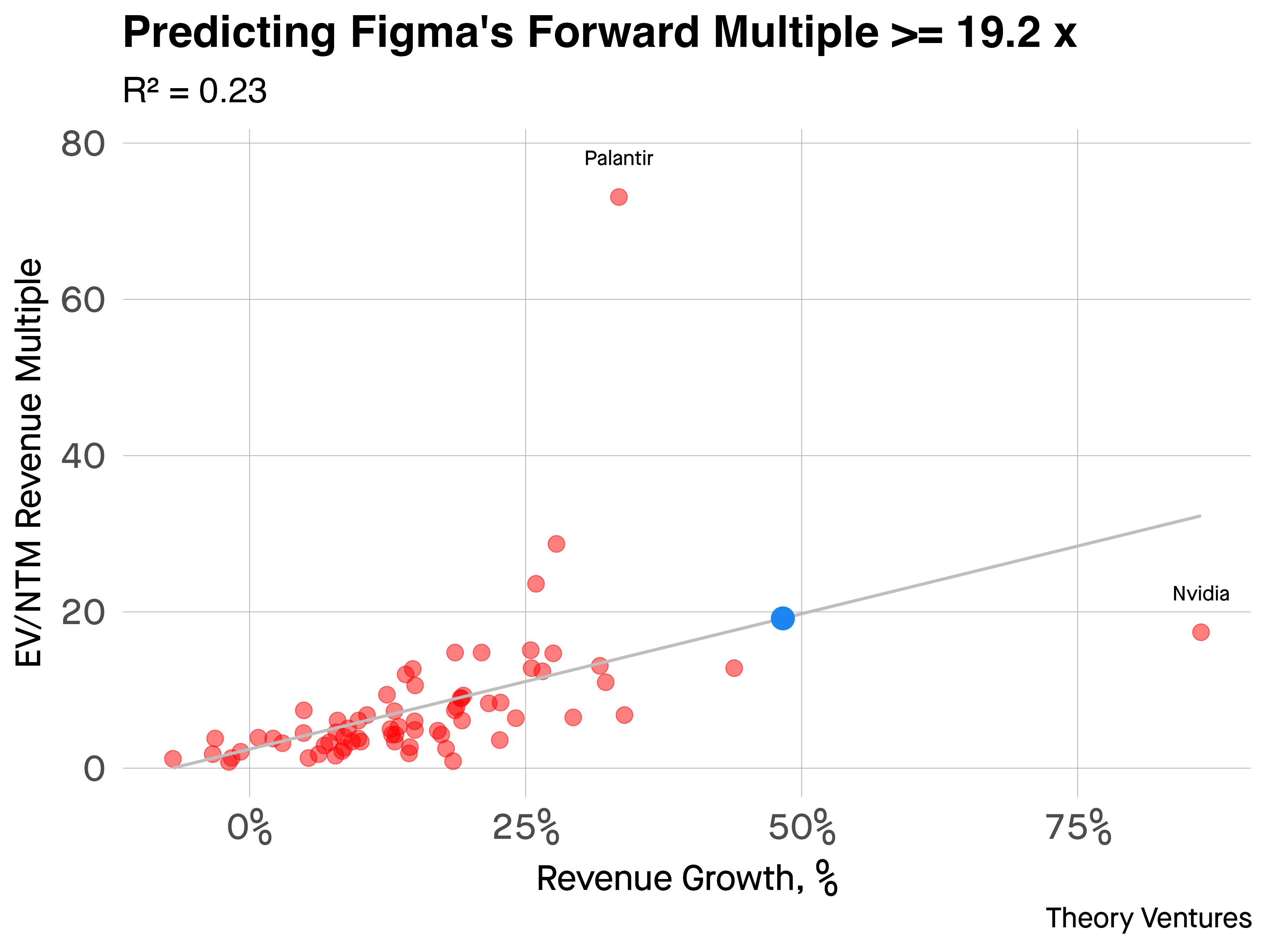

Given its high growth & unique business model, how should the market value Figma? We can use a linear regression based on public SaaS companies to predict its forward revenue multiple. The model shows a modest correlation between revenue growth & valuation multiples (R² = 0.23).

Figma, with its 48% growth, would be the fastest-growing software company in this cohort setting aside NVIDIA. A compelling case can be made that Figma should command a higher-than-predicted valuation. Its combination of hyper-growth, best-in-class sales efficiency, & a passionate, self-propagating user base is rare.

Applying our model’s predicted 19.9x multiple to estimate forward revenue yields an estimated IPO valuation of approximately $21B2 - a premium to the $20B Adobe offered for the company in 2022.

The S-1 tells the story of a category-defining company that built a collaborative design product, developed a phenomenal PLG motion, & is pushing actively into AI.

-

The $1.0 billion termination fee from Adobe was received in December 2023 and recorded as “Other income, net” in Fiscal Year 2024 (ending January 31, 2024). The large stock-based compensation charge of nearly $900 million is related to an employee tender offer in May 2024. Both of these are removed in the non-GAAP data cited above. ↩︎

-

By taking Figma’s 48.3% trailing twelve-month growth rate & discounting it by 15% (to account for a natural growth slowdown), the model produces a forward growth estimate of 41.1%. This would imply forward revenue of about $1.1b. ↩︎